Semiconductor Wafer Inspection Equipment Market by Segments, Country and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

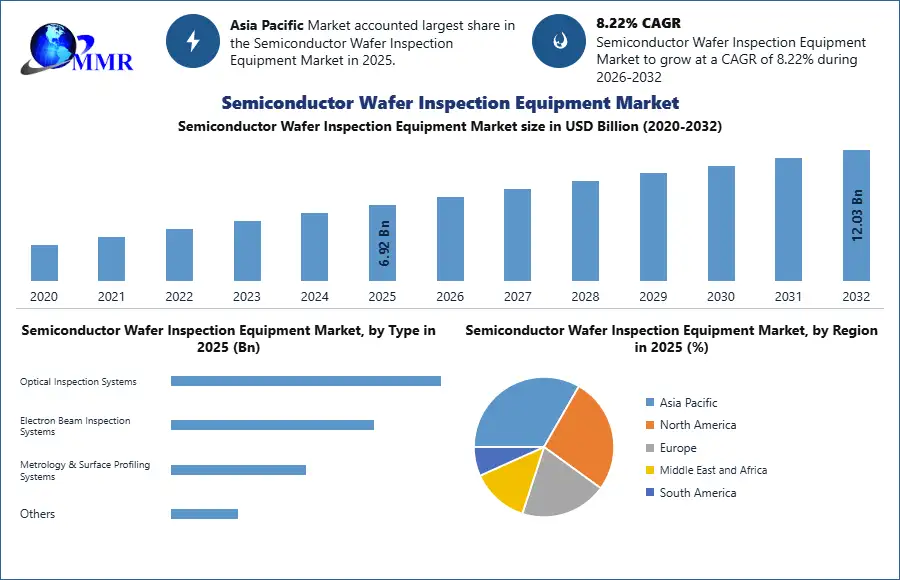

Semiconductor Wafer Inspection Equipment Market size was valued at USD 6.92 Bn in 2025 and the total Semiconductor Wafer Inspection Equipment revenue is expected to grow by 8.22% from 2026 to 2032, reaching nearly USD 12.03 Bn by 2032.

Semiconductor Wafer Inspection Equipment Market Overview

The semiconductor wafer inspection equipment is designed to detect small defects and accurately locate their coordinates automatically. These provide highly consistent and reliable outcomes. The Semiconductor Wafer Inspection Equipment market includes a wide range of equipment and technologies designed to ensure the integrity and performance of semiconductor wafers that are foundational to producing integrated circuits (ICs) and microchips. The demand for high-performance and reliable semiconductor devices has been increasing, which is raising the need for precise wafer inspection to ensure high yields and performance. The advanced wafer inspection systems are expensive and often require significant capital investment.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

As per the study, the Semiconductor Wafer Inspection Equipment market is expected to grow during the forecast period. This is attributed to the increasing demand for high-quality semiconductor devices and applications across various industries.

Semiconductor Wafer Inspection Equipment Market Dynamics

Increasing Investments Driving the Semiconductor Wafer Inspection Equipment Market

The increase in investments in the Semiconductor Wafer Inspection Equipment Market are driving the technological advancements and increasing manufacturing capacity. The advanced inspection tools are being developed because of the capital from industry leaders, governments, and venture capital firms. This is highly maintaining high-quality standards of production. Investments are majorly supporting the creation of sophisticated technologies that detect smaller defects and improve production processes.

For Example:-

1. Nextin is a South Korean semiconductor inspection solution provider that has committed US$200 million to set up operations in Wuxi, Jiangsu province. This strategic investment aims to increase their market share in China and cater to the increasing demand the local semiconductor sector.

Technological Advancements to Drive Semiconductor Wafer Inspection Equipment Market Growth

The wafer inspection sensors including Machine Learning are one of the latest innovations. Machine learning algorithms have been integrated into wafer inspection systems to improve the identification of defects, which are learned from past inspection data and improve defect recognition capabilities over time. This reduces false positives and negatives. Improved optics through high-resolution imaging systems along with advanced lenses and lighting techniques to overcome the challenges of diffraction and scattering is one of the key innovations. This kind of innovations are majorly creating opportunities for the global Semiconductor Wafer Inspection Equipment Market growth.

Hitachi High-Tech Corporation recently launched the LS9300AD, a novel system for the inspection of both sides of non-patterned wafer surfaces for particles and defects. This system combines traditional dark-field laser scattering detection with a new Differential Interference Contrast (DIC) function. This majorly identifies shallow, low-aspect ratio microscopic defects. The LS9300AD uses its existing wafer edge grip and rotating stage methods for comprehensive inspection. It aims to reduce inspection costs and improve yield for semiconductor wafers and device manufacturers. It offers high-sensitivity and high-throughput detection, which are crucial for quality assurance in semiconductor manufacturing processes.

Challenges in Inspection Hinder the Semiconductor Wafer Inspection Equipment Market Growth

The miniaturization in the semiconductor industry introduces major challenges for wafer inspection. As the semiconductor devices are becoming smaller, the once insignificant defects are now severely compromising a device. This is creating demand for sensors that have exceptional sensitivity and precision. The ability to detect minute defects is also hampered due to miniaturization, which has exacerbated light diffraction issues, such as the diffraction limit of optical sensors. Researchers are constantly refining software algorithms and improving optics. The subtle scattering effects complicate defect identification at the nanoscale level. The intricate structures and many layers of modern semiconductor wafers cause interference during the inspection process. Advanced sensors are required to distinguish accurately between true defects and interference to ensure the inspection process remains accurate and efficient.

Semiconductor Wafer Inspection Equipment Market Segment Analysis

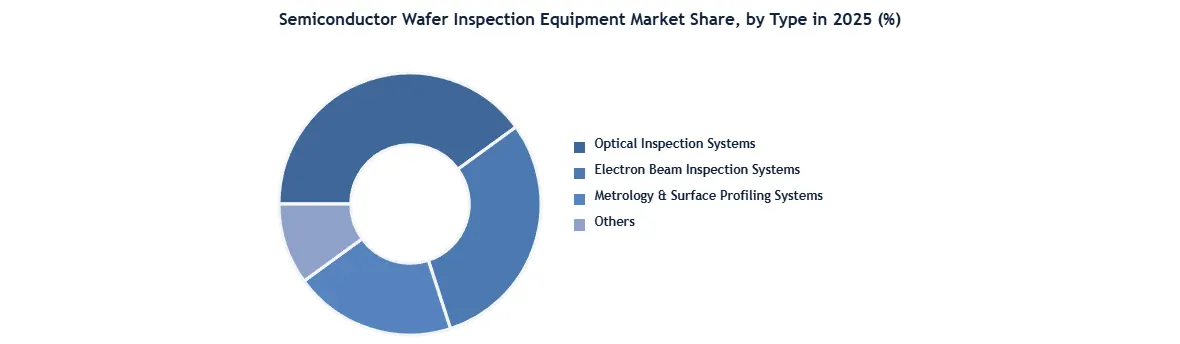

Based on Type: The market is segmented into Optical Inspection Systems, Electron Beam Inspection Systems and Others. The Optical Inspection Systems segment held the largest Semiconductor Wafer Inspection Equipment Market share in 2025. This is attributed to its widespread adoption and efficiency for detecting surface defects and pattern issues on semiconductor wafers. The Electron Beam Inspection Systems accounted the second largest share of the global market in 2025. This is because the system plays a major role in identifying minute defects, ensuring the integrity of advanced semiconductor devices.

Semiconductor Wafer Inspection Equipment Market Regional Insights

Asia Pacific Semiconductor Wafer Inspection Equipment Market dominated the global market in 2025. China held the major share in the regional market. This is attributed to the significant presence of top semiconductor manufacturers, increasing investments by the government in the semiconductor industry and huge demand for consumer electronics. China, South Korea, Japan and Taiwan are the countries that highly benefit from strong semiconductor industries and substantial R&D investments. The need of precise wafer inspection has been rising due to the proliferation of IoT devices, 5G networks, and AI applications for optimal performance and high yield in semiconductor production.

North America Semiconductor Wafer Inspection Equipment Market held the second-largest share in 2025. This is attributed to the significant presence of established players such as KLA Corporation and the rising focus on advanced node technologies with high-performance computing applications. The United States is the key market for Semiconductor Wafer Inspection Equipment, driven by high investments from leading semiconductor manufacturers and strong R&D ecosystem. The need for wafer inspection solutions in the region is majorly being fuelled by the increasing demand for advanced consumer electronics, automotive electronics, and communication devices.

Semiconductor Wafer Inspection Equipment Market Scope: Inquire Before Buying

| Semiconductor Wafer Inspection Equipment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 6.92 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.22% | Market Size in 2032: | 12.03 USD Billion |

| Segments Covered: | by Type | Optical Inspection Systems Electron Beam Inspection Systems Metrology & Surface Profiling Systems Others |

|

| by Inspection Type | Patterned Wafer Inspection Unpatterned Wafer Inspection |

||

| by Wafer Size | 100 mm 150 mm 200 mm 300 mm |

||

| by Application | Defect Inspection Metrology Wafer Edge Inspection Surface Inspection Others |

||

Semiconductor Wafer Inspection Equipment Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Semiconductor Wafer Inspection Equipment Key Players

1. Applied Materials, Inc. (California, USA)

2. Leica Microsystems (Wetzlar, Germany)

3. Hitachi High-Tech Corporation (Tokyo, Japan)

4. KLA Corporation (California, USA)

5. Lam Research Corporation (California, USA)

6. Onto Innovation (Massachusetts, USA)

7. Tokyo Electron Limited (Tokyo, Japan)

8. Veeco Instruments Inc. (New York, USA)

9. Camtek Ltd. (Migdal HaEmek, Israel)

10. Nordson Corporation (Ohio, USA)

11. SCREEN Semiconductor Solutions Co., Ltd. (Kyoto, Japan)

12. ASML Holding N.V. (Veldhoven, Netherlands)

13. Nikon Metrology (Leuven, Belgium)

14. Toray Engineering (Tokyo, Japan)

15. Microtronic (Munich, Germany)

16. Ueno Seiki (Tokyo, Japan)

Others