Artificial Intelligence in Healthcare Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

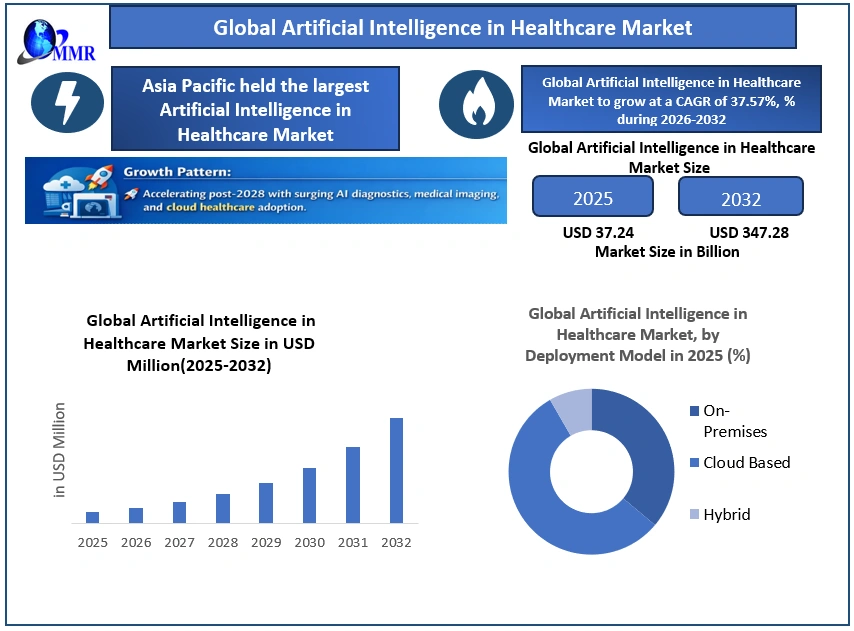

The Global Artificial Intelligence in Healthcare Market is projected to grow from USD 37.24 billion in 2025 to USD 347.28 billion by 2032, registering a CAGR of 37.57% during 2026–2032. This high-growth trajectory reflects the rapid expansion of AI applications beyond diagnostics into enterprise clinical workflows, population health analytics, administrative automation, and cloud-based healthcare intelligence platforms.

Global Artificial Intelligence in Healthcare Market Overview

The Global Artificial Intelligence in Healthcare Market encompasses AI-powered software platforms, clinical decision-support tools, medical imaging analytics, predictive and prescriptive analytics solutions, and cloud-based AI services deployed across healthcare delivery, diagnostics, payer systems, and life sciences workflows. The market excludes standalone medical hardware but includes AI-enabled software integrated with imaging equipment, electronic health records (EHRs), and clinical information systems.

To know about the Research Methodology :- Request Free Sample Report

Artificial Intelligence in Healthcare is transforming care delivery by enabling faster diagnostics, precision medicine, workflow automation, and population-scale analytics. Market growth is supported by rising chronic disease burden, regulatory validation of AI medical devices, expanding digital health infrastructure, and increasing healthcare data availability. Large-scale adoption across hospitals, diagnostic centers, and public health programs is accelerating the transition from pilot deployments to enterprise-scale AI implementation.

Key Highlights :

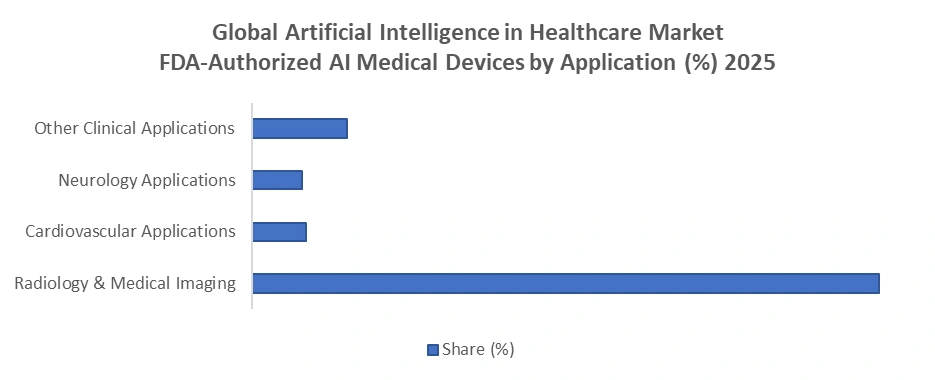

• Over 1,000 AI/ML-enabled medical devices have received U.S. FDA authorization, with approximately 76% concentrated in radiology and medical imaging, indicating strong regulatory acceptance and clinical maturity.

• AI-powered diagnostics and imaging represent the largest and fastest-growing application segment, accounting for over 74% of AI device approvals in 2024, driven by expanding use in CT, MRI, X-ray, and mammography.

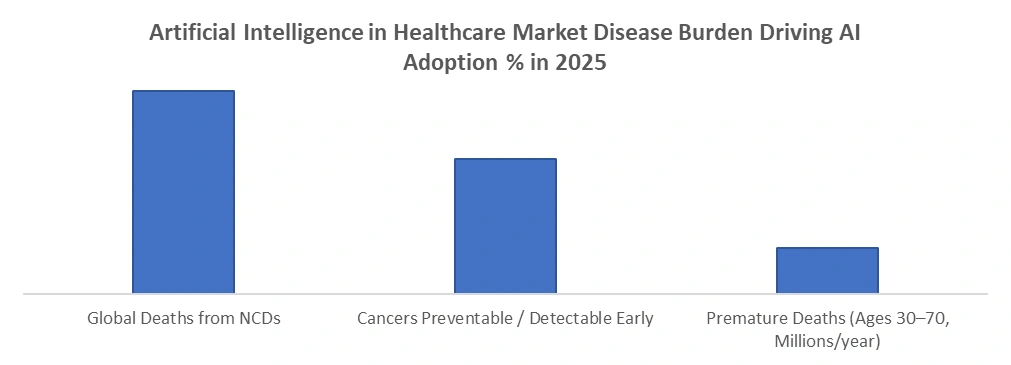

• Noncommunicable diseases account for nearly 75% of global deaths, significantly increasing demand for AI-enabled early detection, screening optimization, and predictive risk analytics.

• Asia Pacific is the fastest-growing region, led by India, where large-scale digital health infrastructure enables population-level AI deployment across diagnostics and public health programs.

• Cloud-based deployment models dominate, accounting for over 60% of new AI healthcare implementations, driven by scalability, faster integration, and lower total cost of owners.

Global Artificial Intelligence in Healthcare Market Dynamics:

AI-Powered Diagnostics and Medical Imaging as the Primary Growth Engine

AI-powered diagnostics and medical imaging are emerging as the primary growth engine of the Global Artificial Intelligence in Healthcare Market, driven by strong regulatory acceptance and accelerating clinical adoption. From a consulting standpoint, extensive regulatory validation has substantially lowered market entry risks, with over 1,000 AI/ML-enabled medical devices authorized in the United States, indicating increasing maturity of AI across clinical workflows. Medical imaging remains the dominant segment within the AI in Healthcare Market, accounting for nearly 76% of authorized AI devices across radiology applications such as X-ray, CT, MRI, ultrasound, and mammography. In 2024, 168 AI-enabled devices received authorization, with 74.4% focused on radiology, while cardiovascular and neurology applications, each representing around 6–7%, signal emerging secondary growth areas.

Global Artificial Intelligence in Healthcare Market: Early Disease Detection Growth

Early disease detection remains a critical demand driver as healthcare systems shift toward preventive and predictive care models. Noncommunicable diseases contribute to nearly 75% of global mortality, while 30–50% of cancers are preventable or detectable at early stages through systematic screening. AI-enabled screening tools improve diagnostic accuracy, throughput, and clinician productivity, particularly in high-volume imaging and pathology environments.

Following a temporary decline during the COVID-19 pandemic, screening utilization rebounded strongly, reaching approximately 79–80% by 2023, reinforcing the role of AI in managing higher screening volumes and addressing workforce shortages.

Global AI in Healthcare Market: Asia Pacific Growth Driven by Scalable Digital Health Infrastructure

Asia Pacific represents the fastest-growing regional market, with India emerging as a strategic deployment hub. Under the Ayushman Bharat Digital Mission (ABDM), India has created a large-scale, AI-ready healthcare data ecosystem, with over 799 million digital health IDs, 670 million linked health records, and extensive provider digitization.

This government-backed digital infrastructure enables scalable deployment of AI diagnostics, population health analytics, and predictive care models, positioning India as a reference market for large-scale AI healthcare implementation in emerging economies.

Data Privacy hamper Global AI in Healthcare Market:

| Key Constraint | Analyst Interpretation | Market-Level Impact |

| Health Data Classified as Highly Sensitive | stringent classification of health data significantly raises compliance thresholds, making large-scale data aggregation for AI model training structurally complex and time-intensive. | Slows innovation cycles and limits scalability of AI diagnostics across regions. |

| Restrictions on Secondary Use of Health Records | limited secondary use of electronic health records reduces dataset diversity, directly affecting the accuracy, generalizability, and clinical validation of AI healthcare models. | Constrains advancement of predictive analytics and population-level AI applications. |

| Fragmented Regulatory Implementation Across Regions | Regulatory inconsistency across jurisdictions introduces legal uncertainty for multinational deployments, increasing operational risk for AI vendors and healthcare providers. | Delays cross-border expansion and discourages uniform AI platform investments. |

Artificial Intelligence Healthcare Segment Market Analysis: Cloud Deployment and AI Applications Driving Adoption

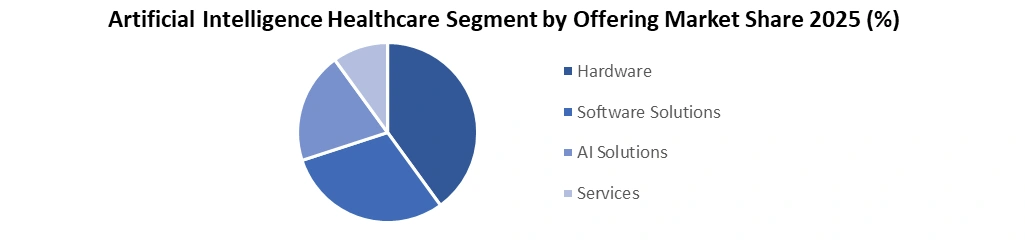

AI in Healthcare Market shows software and AI platforms leading adoption, supported by machine learning frameworks, APIs, and clinical applications integrated with EHRs and imaging systems. GPUs and ASICs dominate hardware demand for imaging and deep learning workloads. Cloud-based deployment holds the largest AI in Healthcare Market share, with hybrid models rising for compliance-sensitive use cases. Diagnosis and early detection remain the leading application. Key players shaping the AI in Healthcare competitive landscape include Microsoft, NVIDIA, GE HealthCare, Siemens Healthiness, Philips, Oracle, Google Health, AWS, Medtronic, Qure.ai, and others.

Global AI in Healthcare Market: Recent Developments by Ethical and Regulatory Compliance .

Stringent classification of health data as highly sensitive significantly increases compliance requirements, making large-scale data aggregation for AI model training complex and time-intensive. Restrictions on secondary use of health records reduce dataset diversity, impacting model generalizability and clinical validation. Additionally, fragmented regulatory implementation across regions introduces legal uncertainty, slowing multinational deployment and increasing operational risk for AI vendors.

Artificial Intelligence in Healthcare Market Scope: Inquiry Before Buying

| Global Artificial Intelligence in Healthcare Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 37.24 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 37.57% | Market Size in 2032: | USD 347.28 Bn. |

| Segments Covered: | by Offering | Hardware Processor MPU FPGA GPU ASIC Memory Network Adapter Interconnect Switch Software Solutions AI platform Application Programming Interfaces(API) Machine Learning Framework AI Solutions Clinical AI Solutions Operational & Administrative AI Solutions Research & Drug Development AI Solutions Services Deployment & Integration Support & Maintenance Others |

|

| by Function | Diagnosis & Early Disease Detection Treatment Planning &Personalization Post-Treatment Surveillance& Survivorship Care Pharmacy Management Data Management &Analytics |

||

| by Deployment Model | On-Premises Cloud Based Hybrid |

||

| by Application | Robot Assisted Surgery Virtual Assistants Administrative Workflow Assistants Connected Medical devices Medical Imaging & Diagnostics Clinical Trials Fraud Detection Others |

||

| by Technology | Machine Learning Deep learning Supervised Unsupervised Others Natural Language Processing Smart Assistance OCR (Optical Character Recognition) Medical Coding & Auto-Coding Text analytics Speech analytics Classification and categorization Context-Aware Computing Computer Vision |

||

| by End User | Healthcare providers Hospitals Clinics Diagnostic Centres Healthcare payers Healthcare companies Patients Others |

||

Artificial Intelligence in Healthcare Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Global Artificial Intelligence in Healthcare Market, Key Players

1) Microsoft

2) Koninklijke Philips N.V.

3) Siemens Healthineers AG

4) Intel Corporation

5) NVIDIA Corporation

6) GE HealthCare Technologies Inc.

7) Medtronic

8) Micron Technology, Inc.

9) Oracle

10) Merative

11) General Vision, Inc.

12) CloudMedx

13) Oncora Medical

14) Lunit Inc.

15) Qure.ai

16) Tempus

17) Babylon Health

18) Stryker

19) Qventus

20) Google Health

21) Amazon Web Services (AWS)

22) BioSymetrics

23) Corti AI

24) Enlitic

25) Others

FAQs – Artificial Intelligence in Healthcare Market

1. What is driving the growth of Artificial Intelligence in Healthcare?

The market is driven by rapid adoption of AI-powered diagnostics, medical imaging, predictive analytics, and cloud-based platforms, supported by regulatory approvals and the rising global burden of chronic diseases.

2. Which application dominates the AI in Healthcare Market?

AI-powered diagnostics and medical imaging dominate the market, accounting for nearly 76% of FDA-authorized AI medical devices, particularly across radiology applications such as CT, MRI, and X-ray imaging.

3. Why is early disease detection a key driver for AI adoption?

Early disease detection is critical as noncommunicable diseases cause nearly 75% of global deaths, and AI enables faster screening, predictive risk modeling, and improved clinical decision-making.

4. Which region is witnessing the fastest growth in AI healthcare adoption?

Asia Pacific is the fastest-growing region, led by India, supported by over 799 million digital health IDs and more than 670 million linked health records enabling large-scale AI deployment.

5. What challenges limit AI adoption in healthcare?

Stringent data privacy regulations such as GDPR and restricted cross-border health data sharing limit large-scale AI model training and slow adoption despite strong technological and clinical demand.